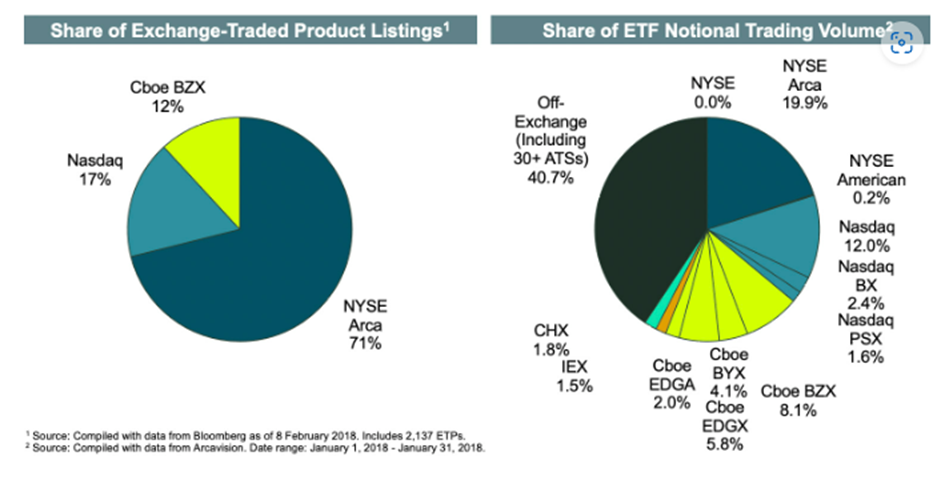

US ETFs: Where They Trade

13 Exchanges, 30+ Alternative Trading Systems (ATSs), and many other non-Exchange locations.

U.S. regulators have sought to facilitate a balanced market structure that promotes competition among trading venues while ensuring linkages between trading venues to provide the opportunity for investor orders to be fulfilled.

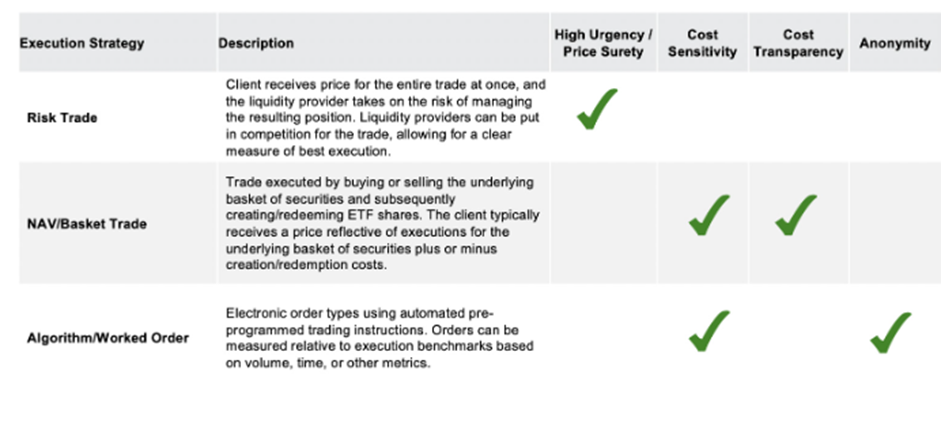

ETF Execution Strategies

Overview of ETF execution strategies for institutional-sized orders.

Additional considerations include the size of the trade, the secondary liquidity of the ETF, the time of day, volatility, and the structure of the underlying stock market.

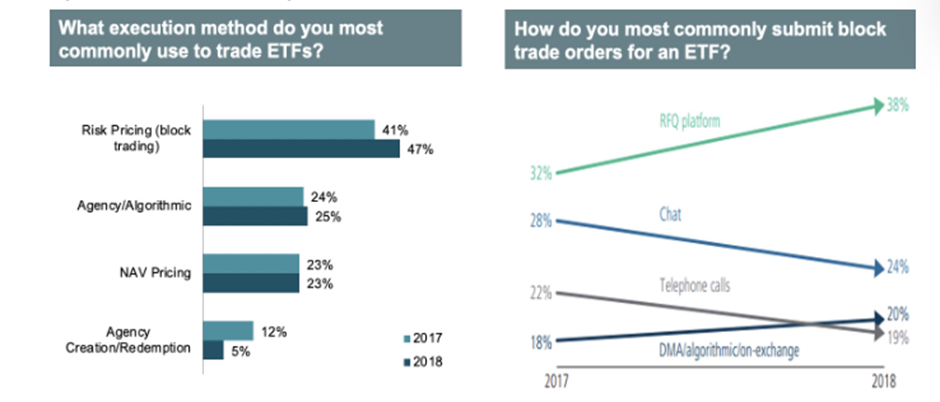

Increased use of RFQ platforms for block operations.

U.S. ETF: Tied to market structure

There are four main types of links that connect U.S. stock trading venues, ensuring that competition between trading venues does not undermine the opportunity for investors’ orders to meet directly.

Trading Venue Links

- Rule of Exchange: Rule 611 of the NMS regulation, known as the “swap rule” or “order protection rule”, forces price competition on trading venues in two ways: It restricts trades so that they do not occur at prices worse than the best prices displayed in the market ensures that the best displayed quotes in the market are not overlooked by trades at lower prices.

- Consolidated Market Data: Consolidated market data allows trading firms to build a consolidated view of order and trade data from multiple locations and thus determine where to route orders.

- Best Execution: The legal duty of best execution brokers requires them to obtain the most favorable terms available when executing orders by routing orders.

- Intelligent Order Routing Technology: Brokers have trading incentives to provide high-quality order routing technology to ensure that they access liquidity across the various trading venues in an optimal manner for their clients.